Analysis of industry trends in the first half of 2024: Ethereum still dominates, and Asian and African startups hit a new high

Original author: @QwQiao @xyczzcyx

Compiled by: TechFlow

At @alliancedao , we receive around 3,000 applications per year to join our crypto startup accelerator. We collect data such as the blockchain they use, product type, and geographic location. Because of the large sample size and our neutrality to these factors, we are able to gain unique insights into how the industry is trending.

Blockchain

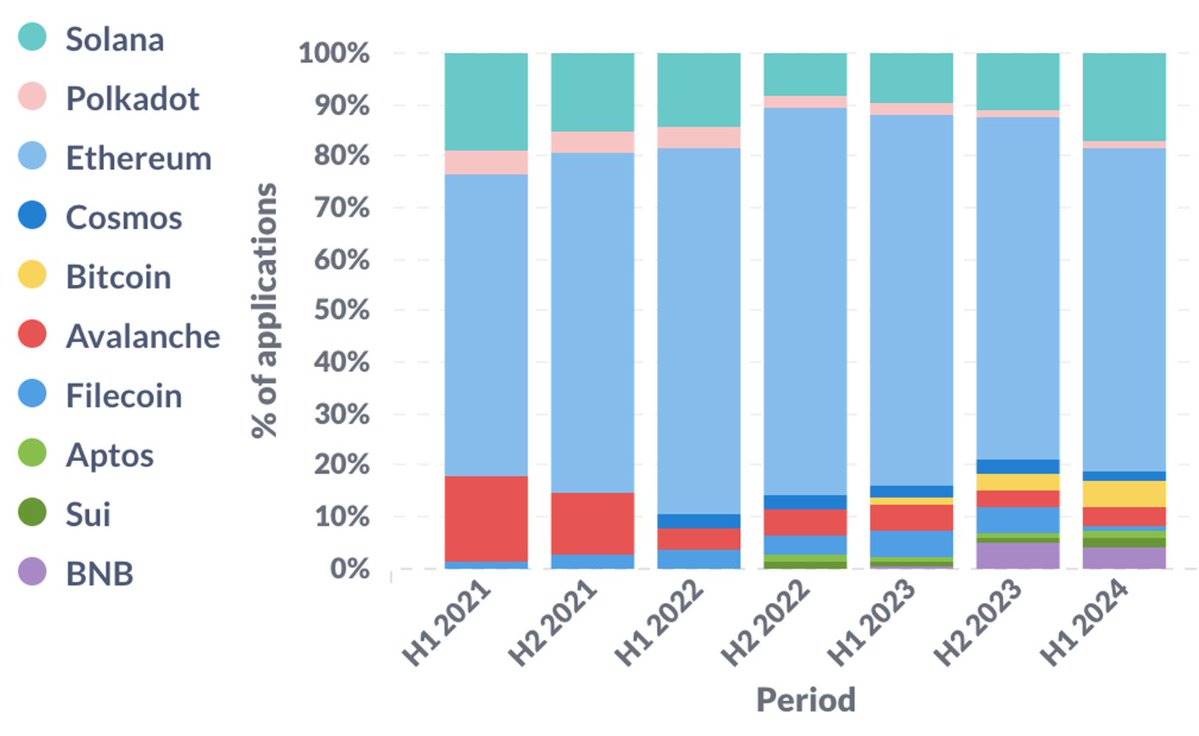

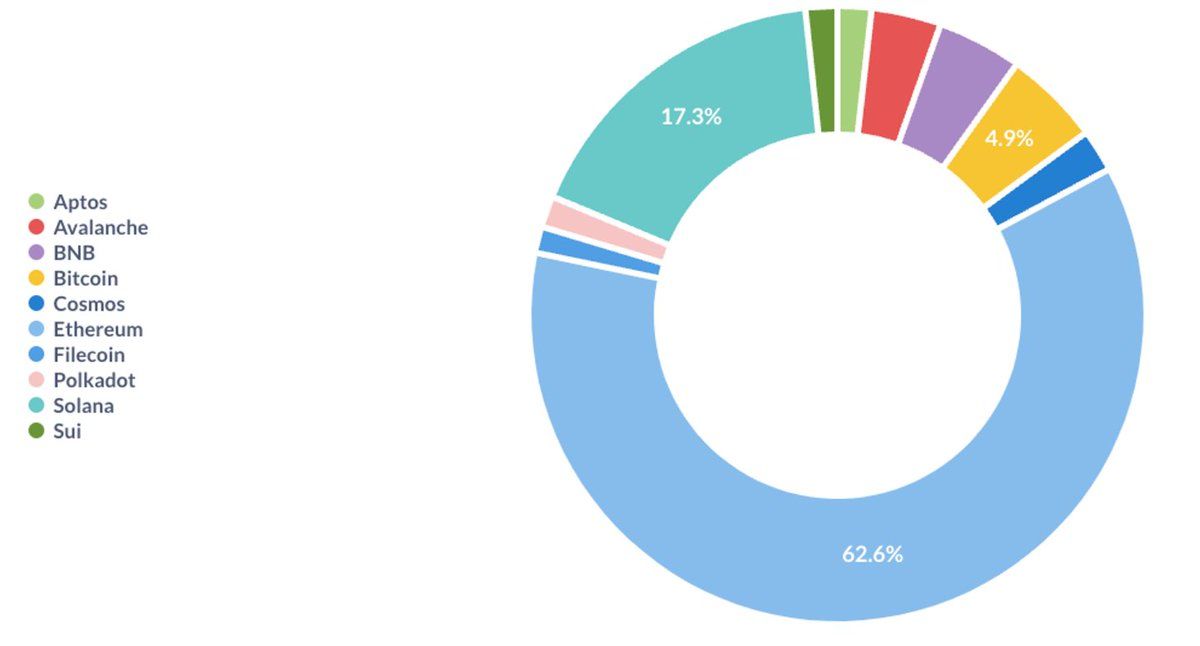

Layer 1

Ethereum remains the dominant ecosystem. However, Solana is recovering after bottoming out in the second half of 2022, which may be related to the collapse of FTX in the same period. Bitcoin is experiencing a resurgence amid the craze for ordinarys, runes, and Bitcoin L2 technology.

Changes in L1 share over time

L1 share in the first half of 2024

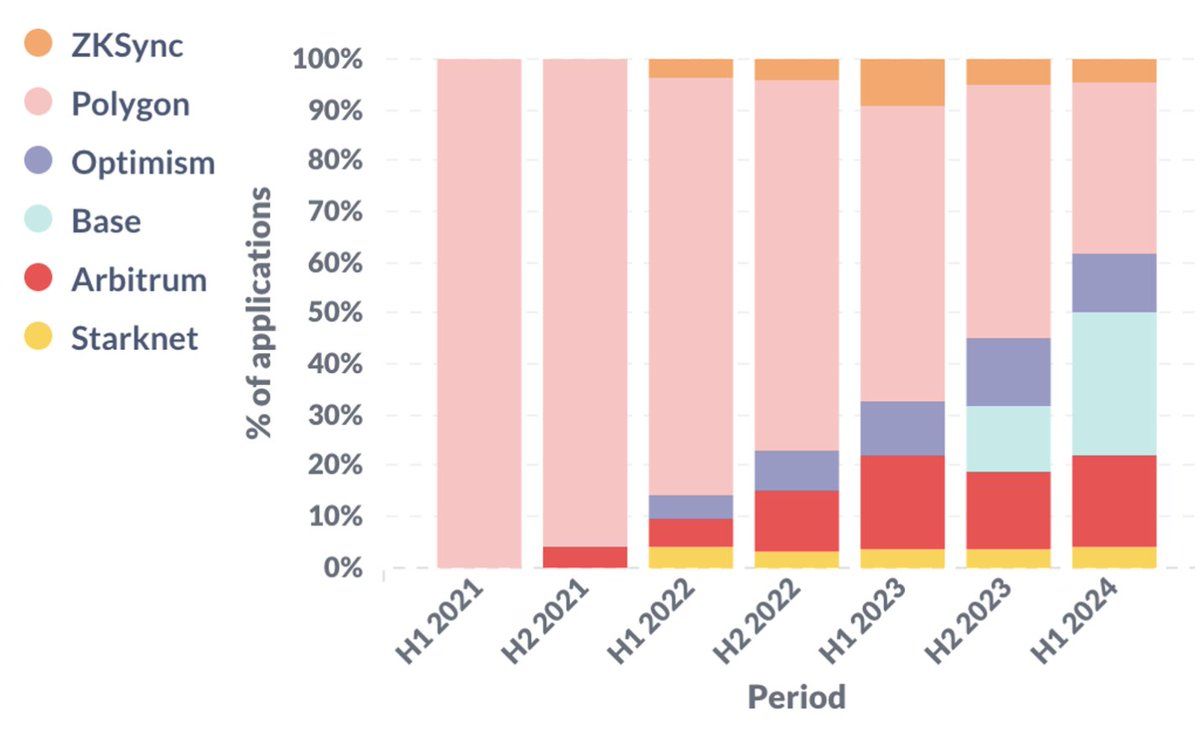

Ethereum Layer 2

Focus on Ethereum L2 (and sidechains). Over the past 3 years, Optimistic rollups have gradually gained more attention. Notably, in the first half of 2024, Base accounted for more than a quarter of startups built on Ethereum L2.

Changes in L2 over time

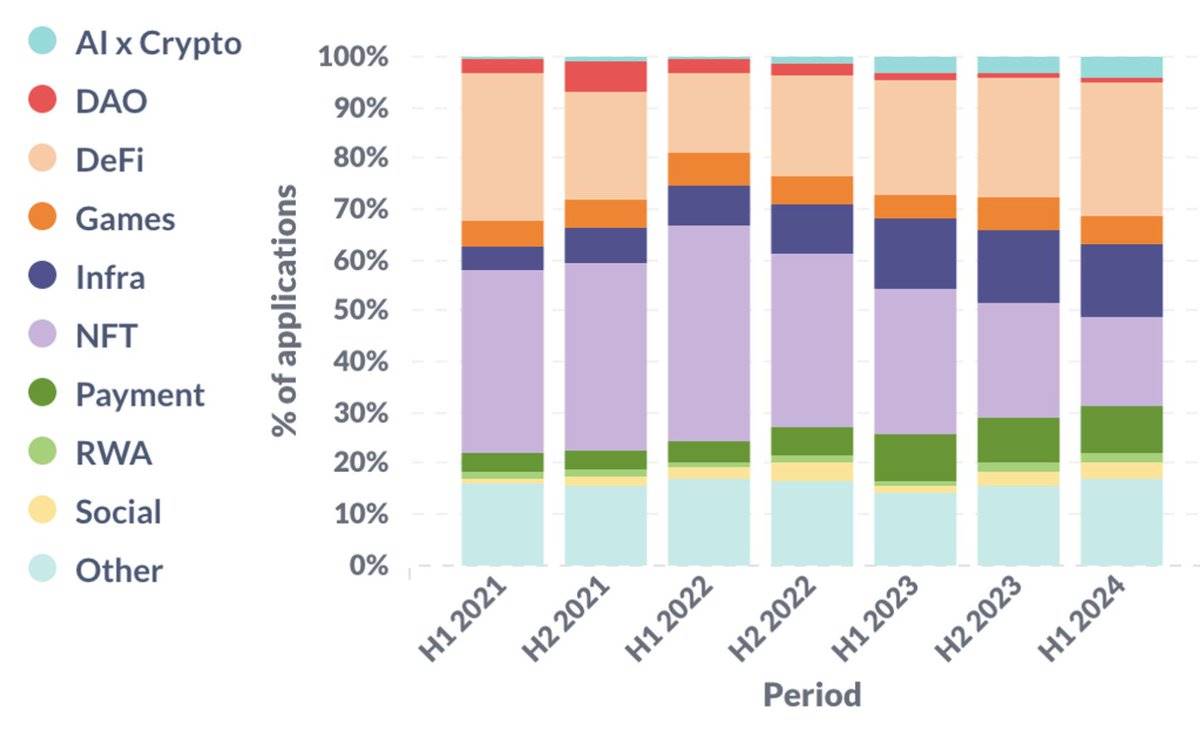

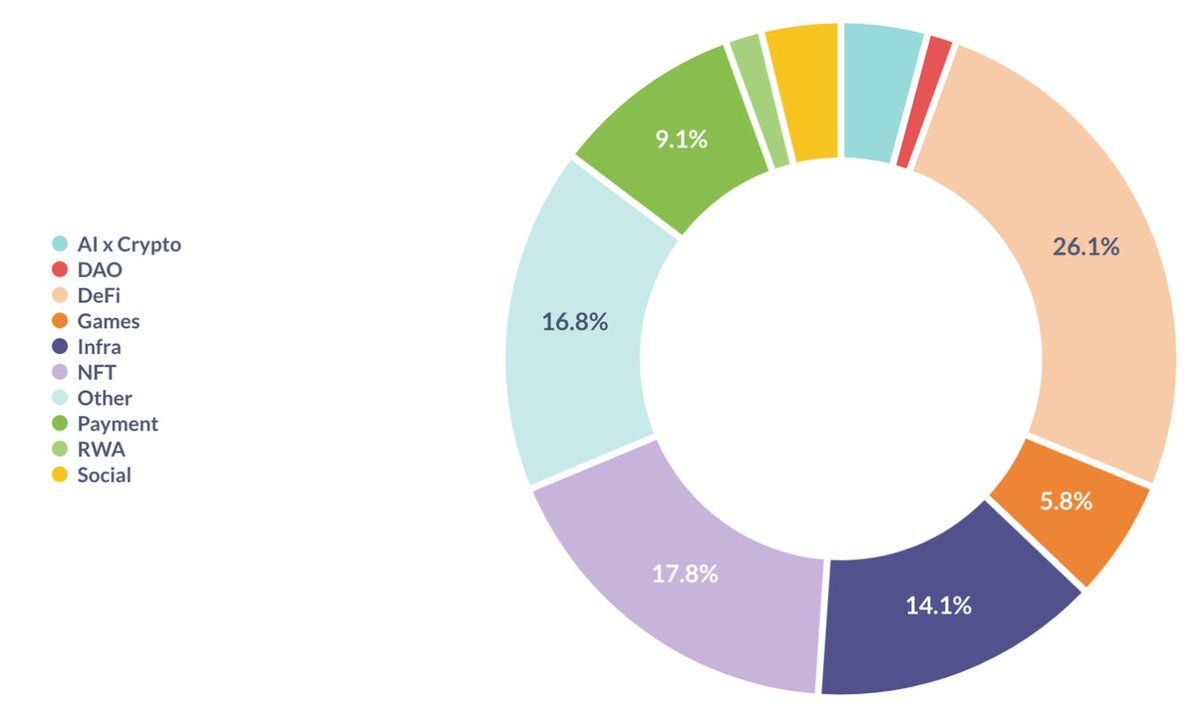

Product Trends

An increasing number of startups are focusing on infrastructure, DeFi, payments, and the combination of AI and cryptocurrencies, often at the expense of NFTs. In these areas, the development of infrastructure and AI is consistent with the trend of public discussion. However, the rise of DeFi and payments may surprise many people because there is hardly much public attention on them. Coincidentally, we believe that these two areas are also one of the few verticals in which cryptocurrencies have found clear product-market fit (PMF).

Changes in product share over time

Product share in the first half of 2024

Note that this is an imperfect way to categorize products, as these categories are not mutually exclusive. For example, a startup may operate in both the gaming and NFT space, in which case we would assign a weight of 0.5 to both gaming and NFT.

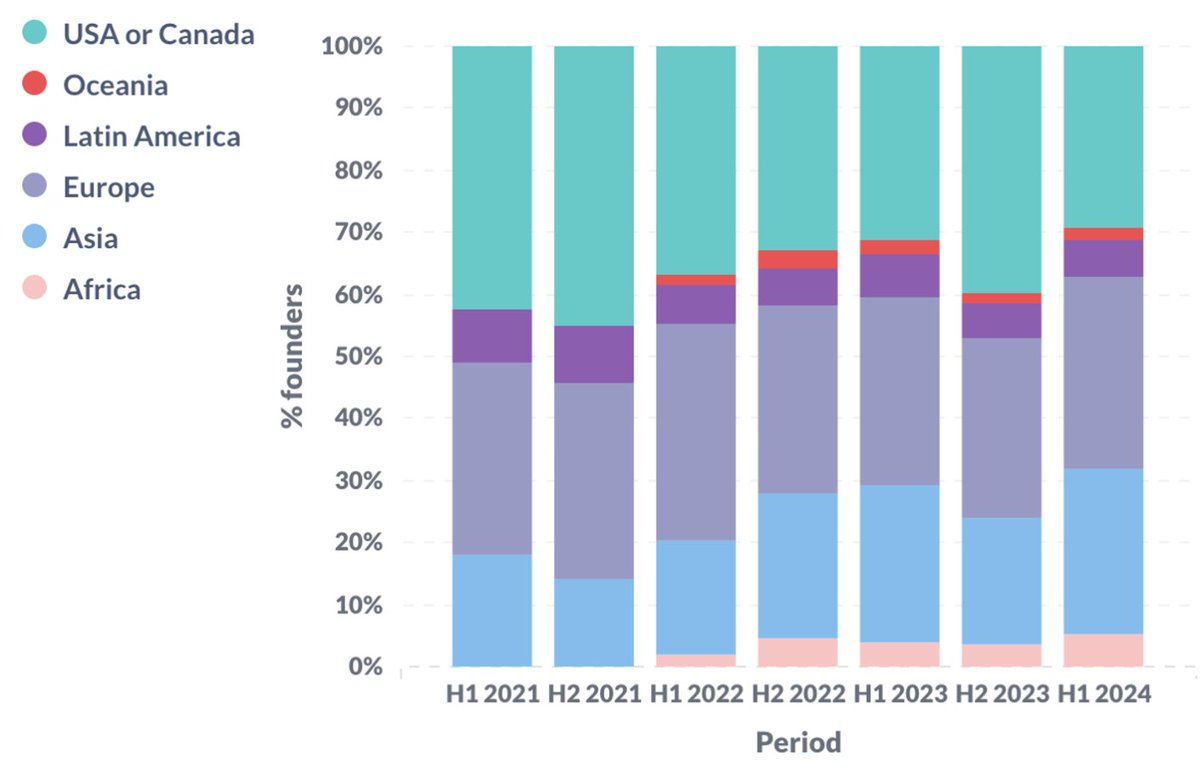

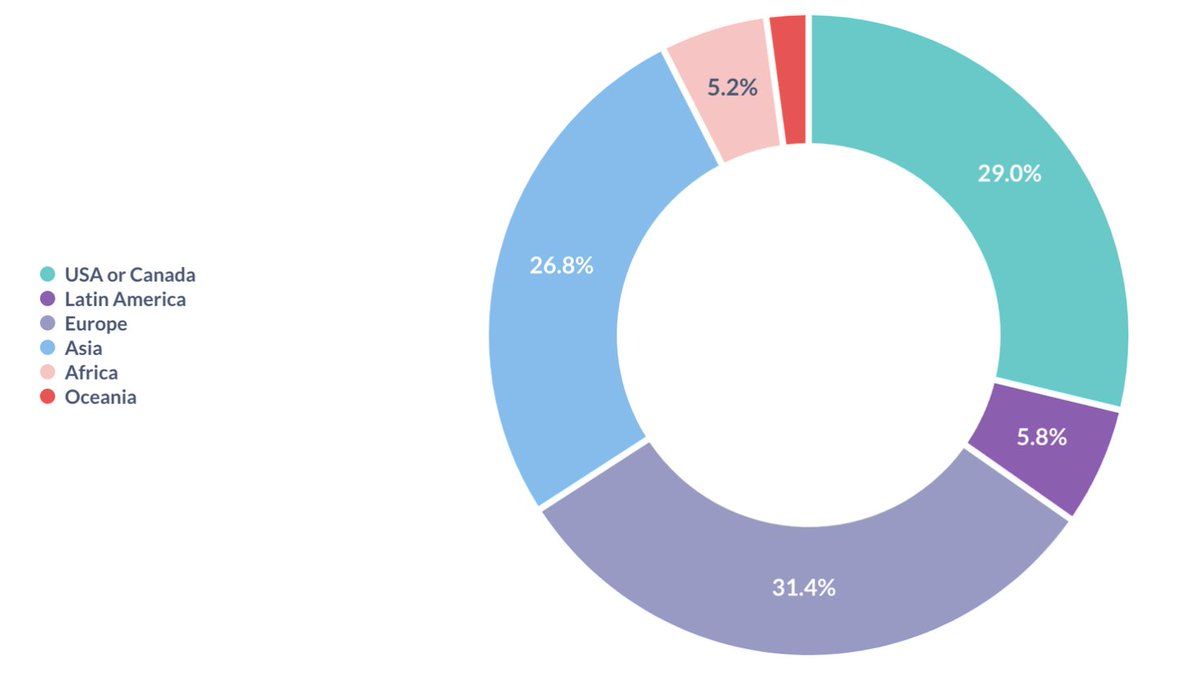

Geographical distribution

In the first half of 2024, we see a record low percentage of startups from the US and Canada, and a record high percentage of startups from Asia and Africa. This is likely due to 1) increased regulatory uncertainty in the US, and 2) increased real-world adoption of cryptocurrencies in emerging markets.

Overall, North America, Europe and Asia remain the three major regions, each contributing 1/4 to 1/3 of all startups.

Geographical changes over time

Geographical distribution in the first half of 2024

What starts here may be more appealing to founders and VCs. If you are one of them, keep reading.

Founder Background

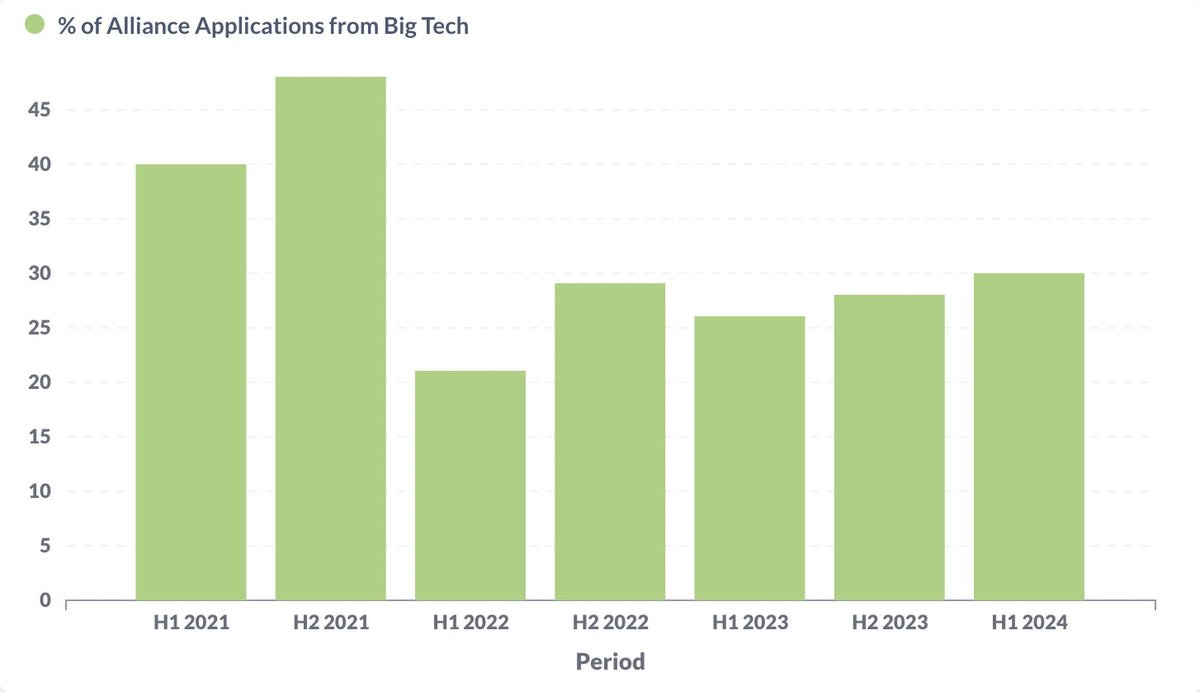

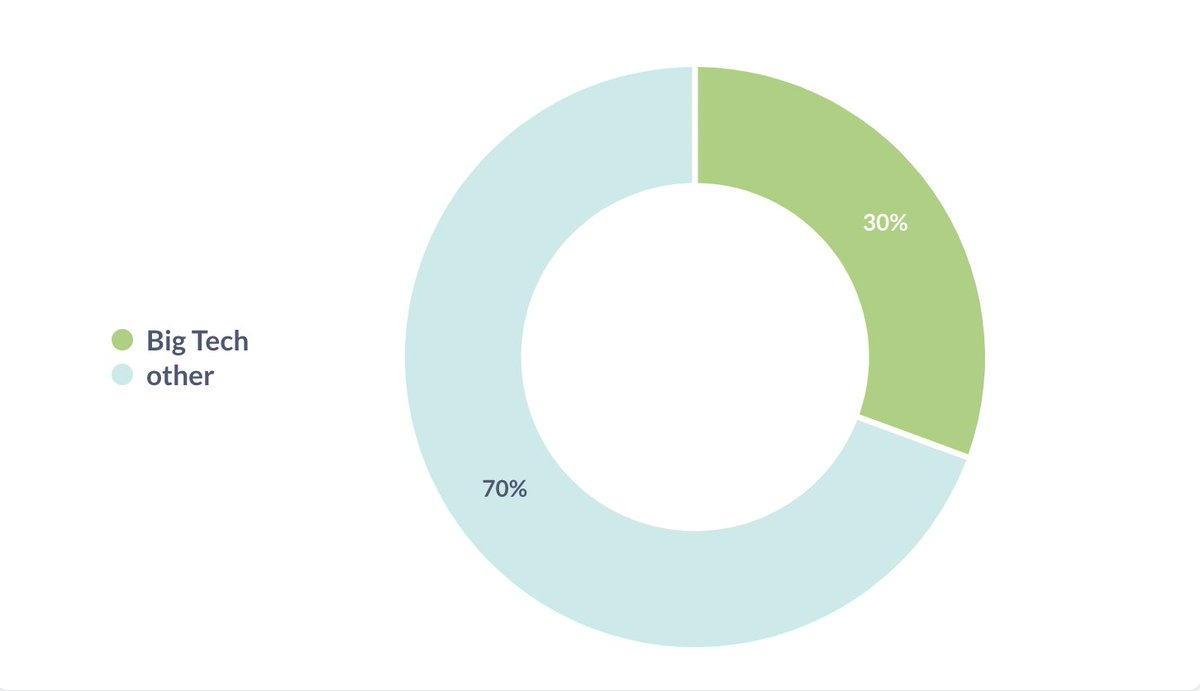

Big Tech

The percentage of founders with a Big Tech background peaked in 2021 and is currently at 30%. We define Big Tech as the tech companies in the SP 500. The exact definition is not important; what matters is the trend over time.

Percentage of founders with a background in large technology companies over time

Proportion of founders from large technology companies in the first half of 2024

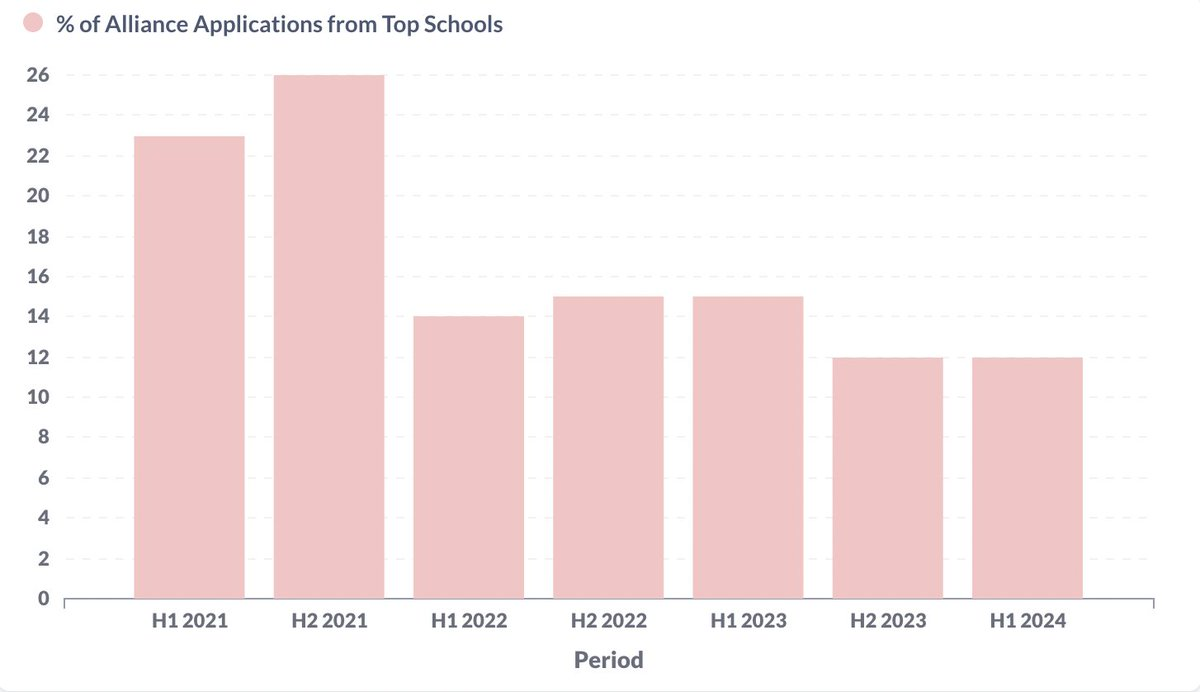

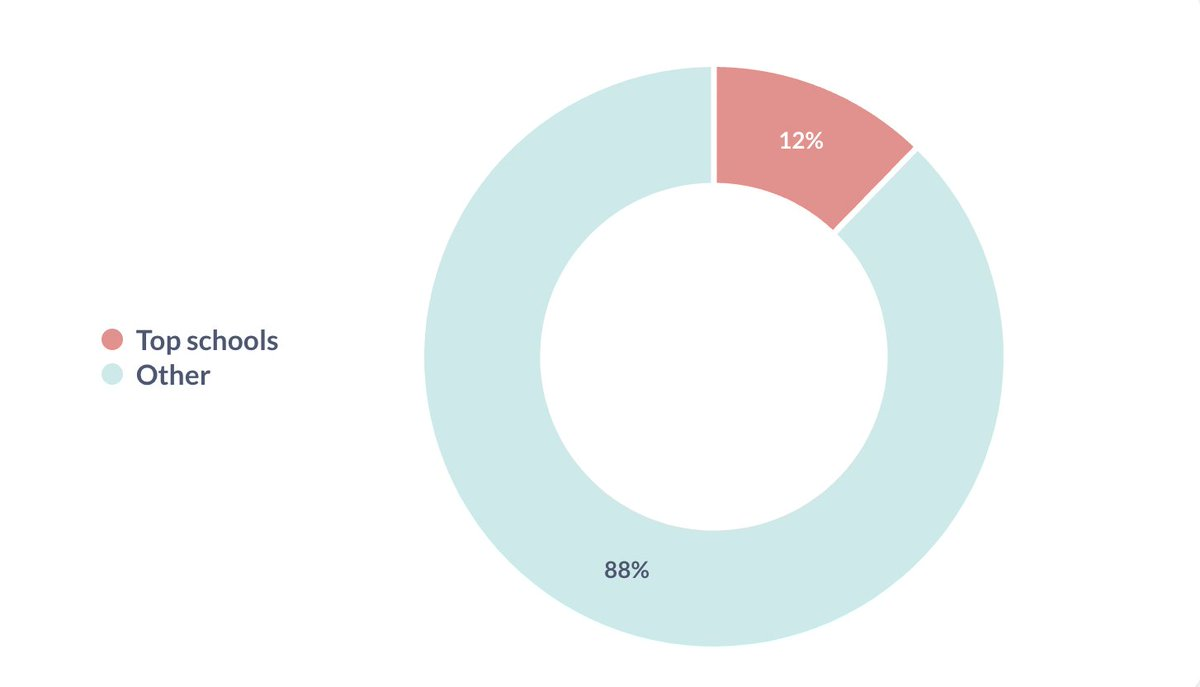

Top universities

Likewise, the percentage of founders graduating from top universities peaked in 2021. We define top universities as the QS world’s top 100 universities.

Percentage of founders graduating from top schools over time

Proportion of founders graduating from top universities in the first half of 2024

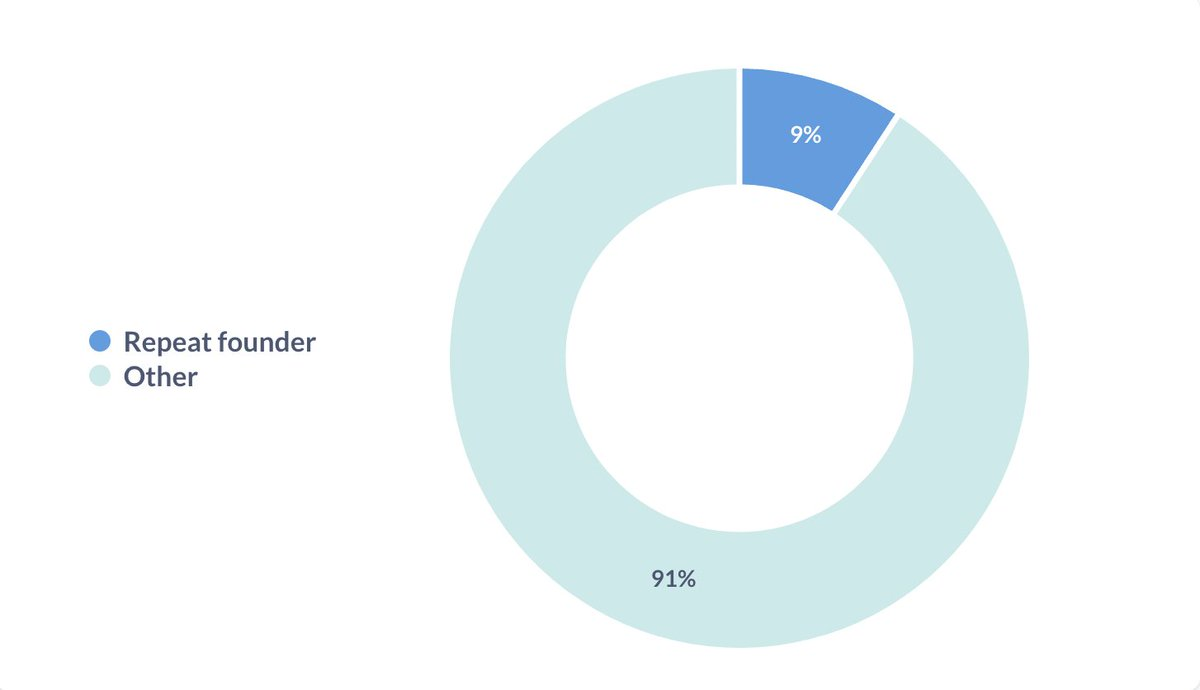

Repeat founder

About 1 in 10 founders had previously founded a startup.

Repeat founder

Team Composition

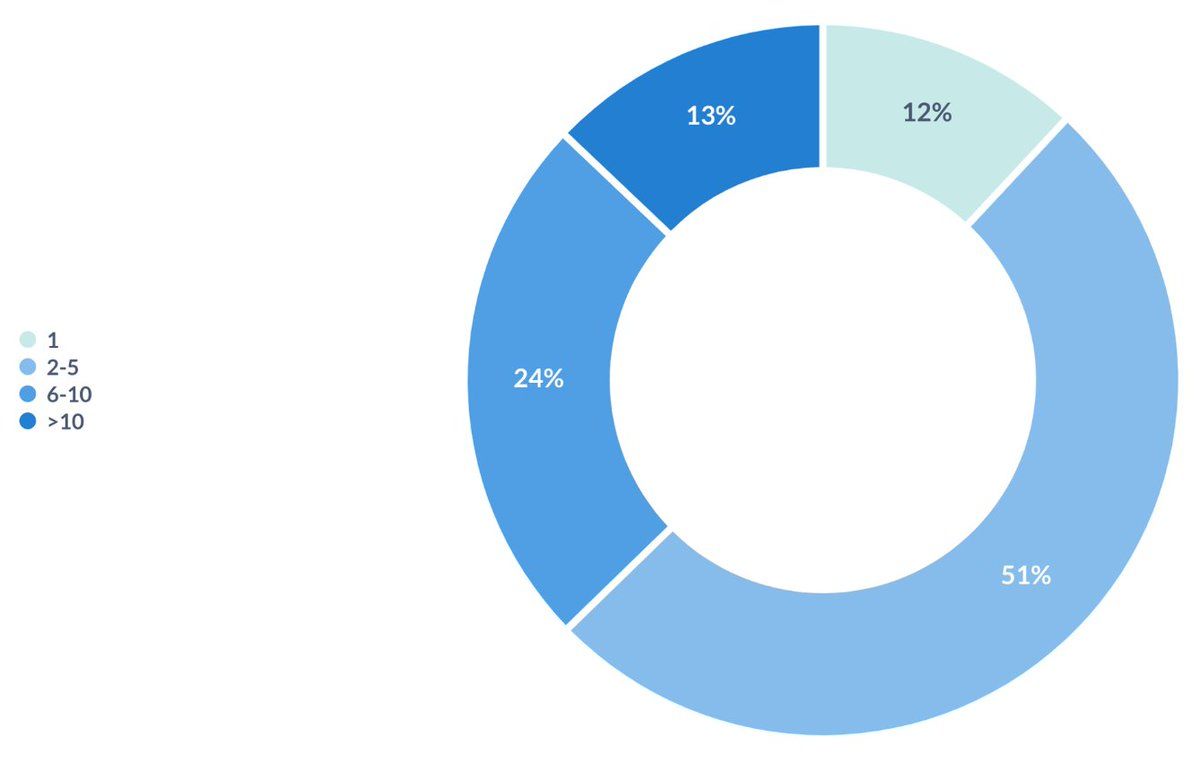

Team size

More than half of startups have a team size between 2 and 5 people. We believe this is the optimal size for pre-market fit (PMF) startups.

Team size

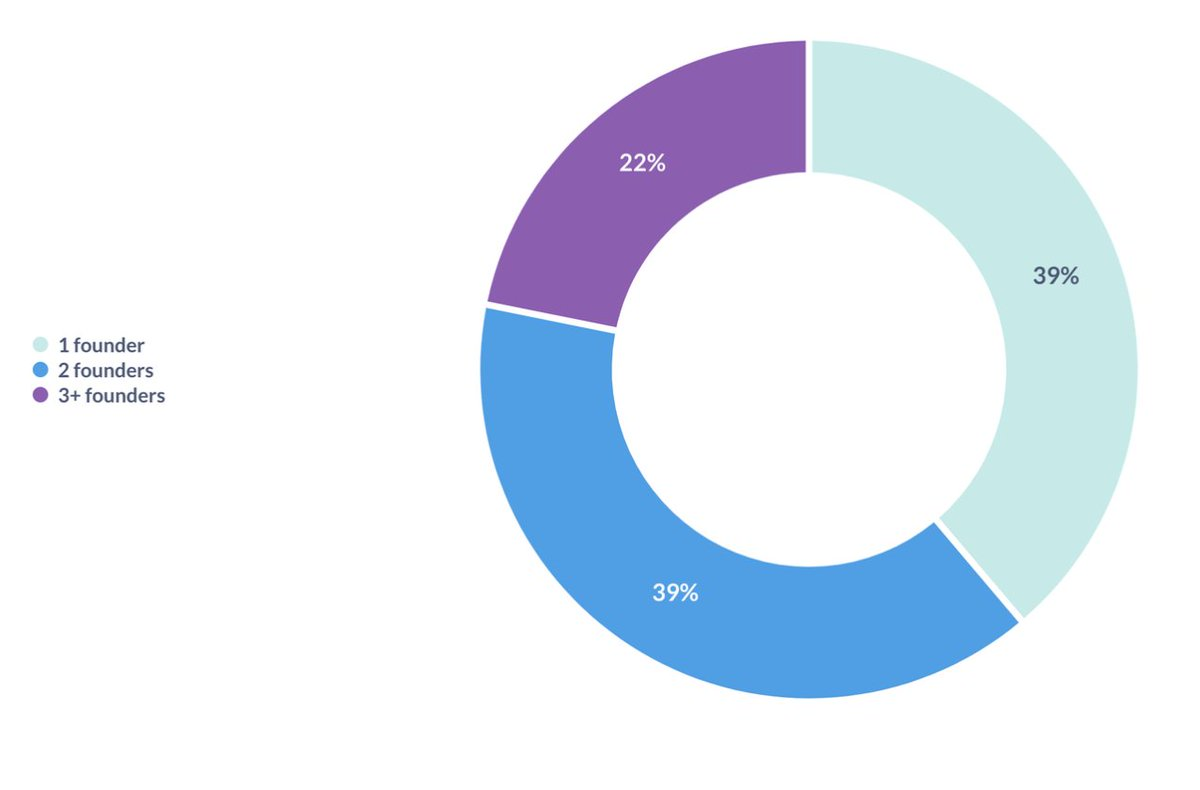

Number of co-founders

Less than 40% of startups are founded by a single founder. For reference, various studies show that 20-30% of unicorns were founded by a single founder.

Number of founders

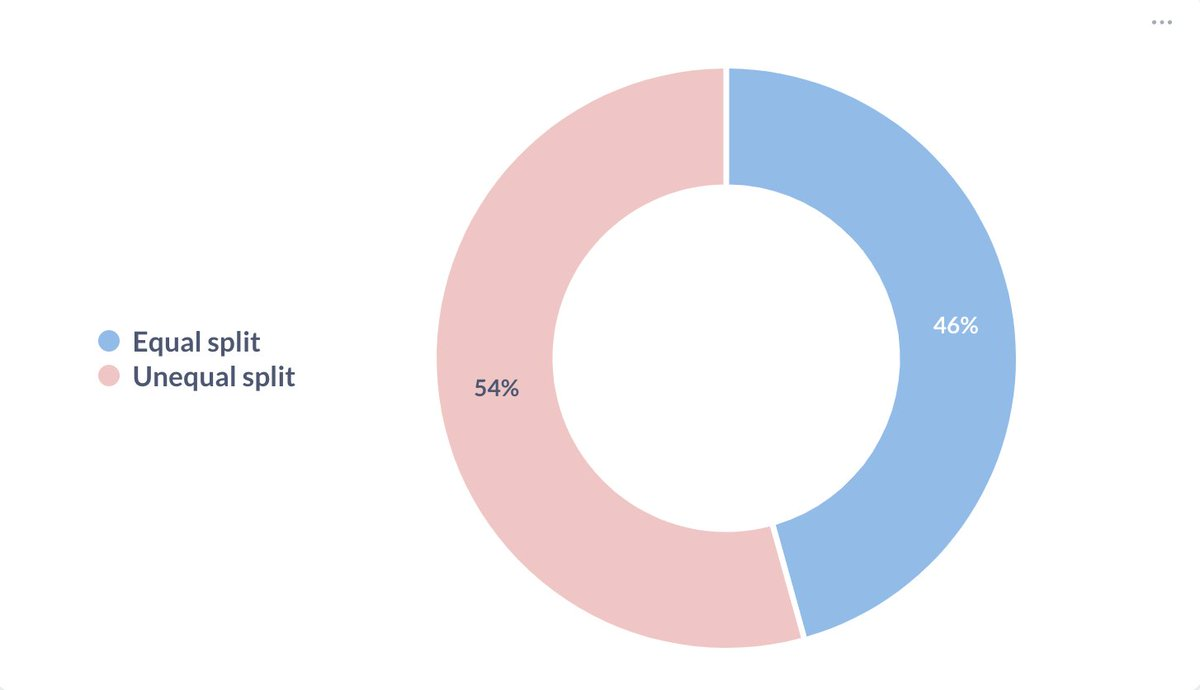

Equity Distribution

Among startups with two or more co-founders, about half split the equity equally, while the other half do not.

Equity Distribution

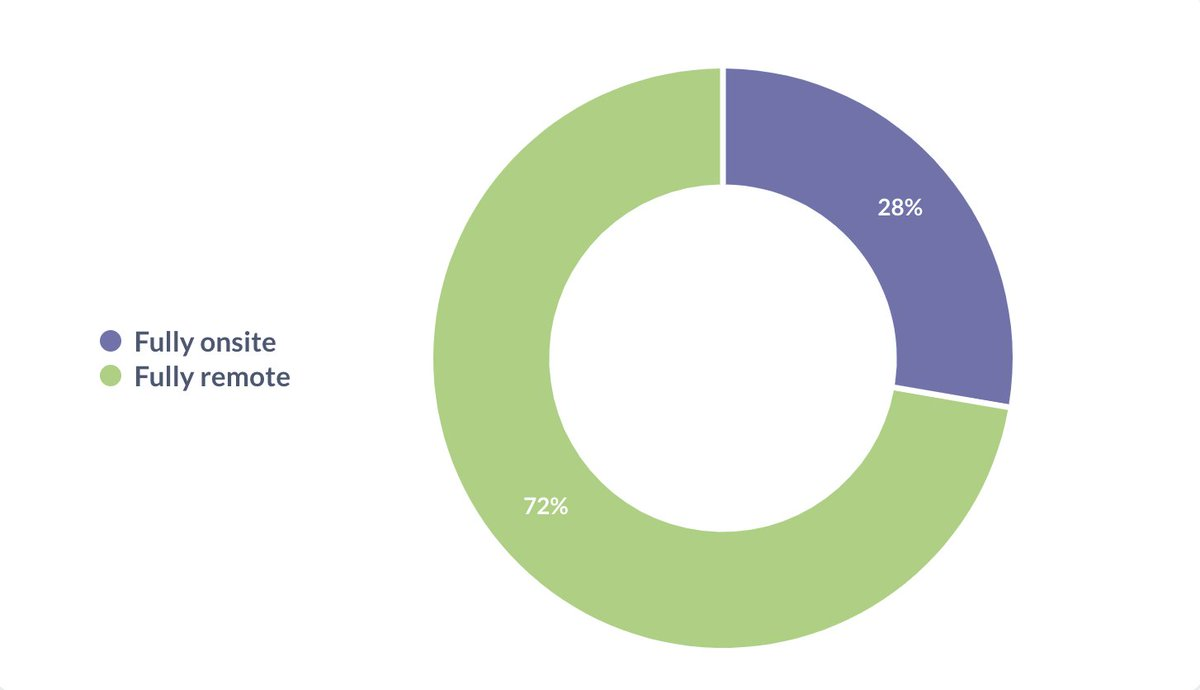

Remote work

Nearly three-quarters of startups adopt a completely remote work model.

Remote work

Original link

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Cobie: Long-term trading

Crypto Twitter doesn't want to hear "get rich in ten years" stories. But that might actually be the only truly viable way.

The central bank sets a major tone on stablecoins for the first time—where will the market go from here?

This statement will not directly affect the Hong Kong stablecoin market, but it will have an indirect impact, as mainland institutions will enter the Hong Kong stablecoin market more cautiously and low-key.

Charlie Munger's Final Years: Bold Investments at 99, Supporting Young Neighbors to Build a Real Estate Empire

A few days before his death, Munger asked his family to leave the hospital room so he could make one last call to Buffett. The two legendary partners then bid their final farewell.

Stacks Nakamoto Upgrade

STX has never missed out on market speculation surrounding the BTC ecosystem, but previous hype was more like "castles in the air" without a solid foundation. After the Nakamoto upgrade, Stacks will provide the market with higher expectations through improved performance and sBTC.